There is a familiar phrase often used in business, construction, consulting, and professional services:

“You can have it good, fast, or cheap. Pick any two.”

At first glance, it sounds simple.

But underneath it is one of the most important truths in business, life, and financial planning:

Every meaningful decision involves tradeoffs.

If you want something good and fast, it usually will not be cheap.

If you want something good and cheap, it usually will not be fast.

If you want something fast and cheap, quality often suffers.

Most people understand this immediately because they have seen it in real life. It applies to building a house, hiring a professional, running a business, making a medical decision, or solving a family problem.

But could this same principle also apply when it comes to:

- wealth management,

- financial planning,

- retirement,

- protection,

- and legacy planning?

At Ametrine Wealth Strategies, we believe it often does.

We call this concept:

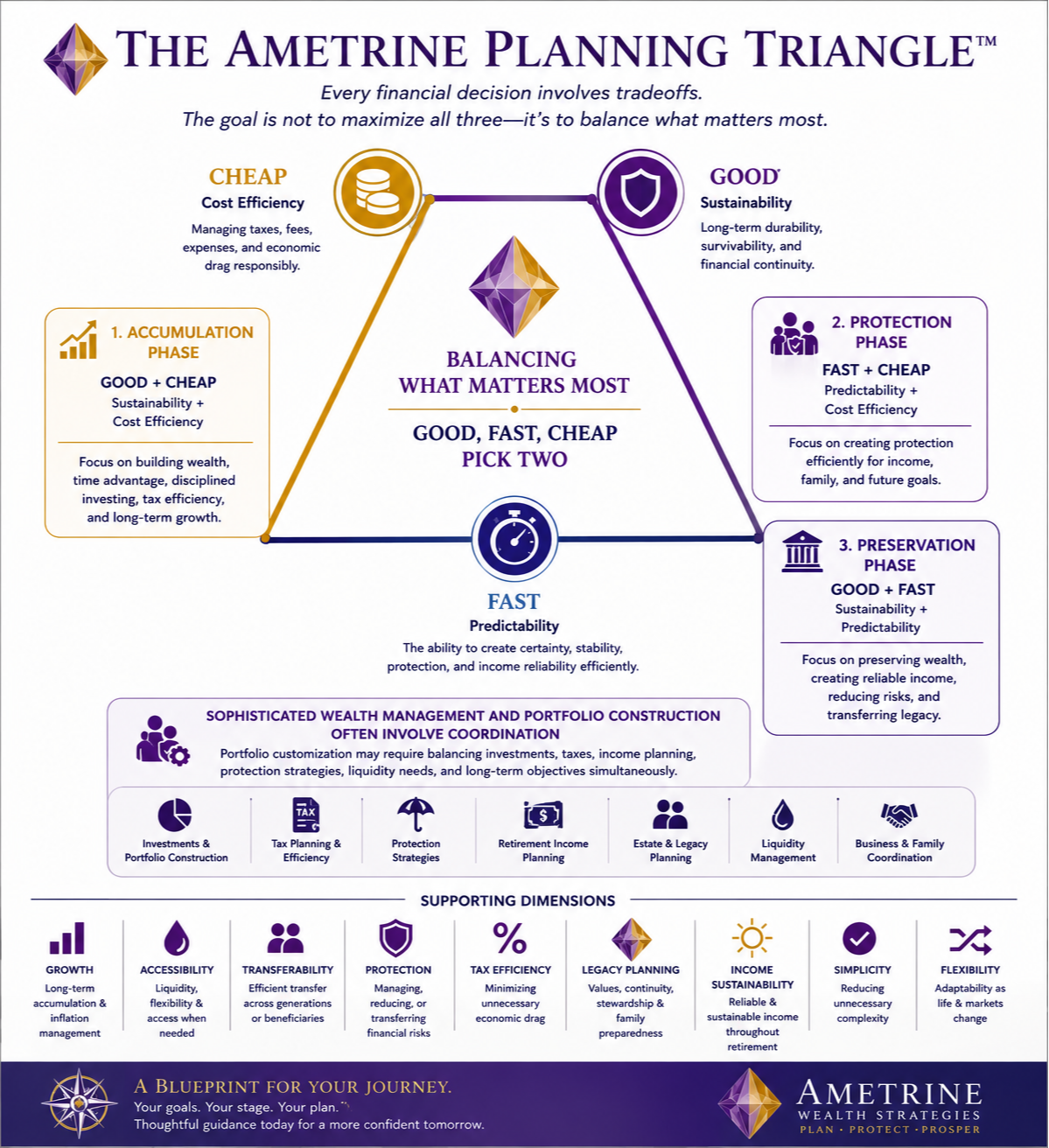

The Ametrine Planning Triangle™

The traditional business framework is usually understood this way:

Traditional Concept | Traditional Meaning |

Good | High quality |

Fast | Speed |

Cheap | Low cost |

But in financial planning, these ideas may require a deeper interpretation.

Traditional Concept | Ametrine Interpretation | Financial Meaning |

Good | Sustainability | Long-term durability, survivability, and financial continuity |

Fast | Predictability | The ability to establish protection, certainty, stability, or income reliability efficiently |

Cheap | Cost Efficiency | Managing taxes, fees, expenses, and economic drag responsibly |

The Ametrine Financial Triangle

The goal is not necessarily to maximize all three simultaneously.

The goal is understanding:

- what you are prioritizing,

- what tradeoffs exist,

- and which balance may be most appropriate for your stage of life, level of risk, family responsibilities, and long-term goals.

Financial Planning Is Often the Management of Tradeoffs

Many people naturally want:

- high returns,

- low risk,

- low taxes,

- full liquidity,

- guarantees,

- simplicity,

- flexibility,

- and immediate results.

But financial strategies rarely maximize every objective at once.

Higher growth may involve greater volatility. Greater predictability may reduce upside potential. Full liquidity may reduce long-term efficiency. Lower taxes today may create future limitations. The lowest-cost option may reduce flexibility, coordination, or protection.

That does not mean one choice is always right and another is always wrong.

It means sophisticated planning often begins when tradeoffs become visible.

Growth vs. Stability

One of the most common tradeoffs in financial planning is growth versus stability.

Strategies focused heavily on growth may help support long-term accumulation and inflation protection, but they may also involve volatility and uncertainty.

Strategies focused heavily on stability and predictability may provide more structure, income reliability, or protection, but they may also reduce upside potential or flexibility.

Neither approach is universally right or wrong.

The appropriate balance depends on:

- age,

- time horizon,

- retirement objectives,

- family responsibilities,

- income needs,

- liquidity needs,

- and overall financial structure.

This is why financial planning should not be about maximizing one variable.

It should be about balancing multiple competing priorities intentionally over time.

The Accumulation Phase

“Good” + “Cheap”

Sustainability + Cost Efficiency

When people are younger and building wealth, time is often their greatest asset.

At this stage, planning may emphasize:

- disciplined accumulation,

- long-term investing,

- tax efficiency,

- lower costs,

- and sustainable growth.

Predictability may matter less because time itself can act as a shock absorber.

For many younger investors, patience, consistency, and cost-conscious investing may become powerful tools.

But even here, tradeoffs exist. Growth is not guaranteed. Markets fluctuate. Low cost alone does not necessarily mean a strategy is appropriate. Sustainability still requires discipline, structure, and long-term planning.

The Protection Phase

“Fast” + “Cheap”

Predictability + Cost Efficiency

As life responsibilities increase, the planning conversation often changes.

Marriage, children, mortgages, business obligations, income dependency, and family responsibilities can make protection more important.

This is where strategies such as:

- life insurance,

- disability insurance,

- emergency reserves,

- long-term care planning,

- and other risk-transfer tools

may help create immediate financial predictability.

As many advisors have said throughout the years:

“With the stroke of a pen, you can create an estate.”

For a young family still building wealth, proper protection can sometimes become one of the fastest and most cost-efficient ways to create financial continuity.

If death, disability, illness, or unexpected disruption occurs, protection strategies may help preserve:

- income,

- family stability,

- long-term goals,

- and financial dignity.

This is where “fast” does not mean rushed or careless.

It may mean that protection can be established efficiently during the appropriate planning window before a major risk occurs.

At this stage, predictability may matter more than maximizing returns alone.

The Preservation Phase

“Good” + “Fast”

Sustainability + Predictability

As wealth grows and retirement approaches, priorities often shift again.

Now the concerns may include:

- sequence-of-returns risk,

- income reliability,

- healthcare costs,

- taxes,

- estate planning,

- surviving spouse protection,

- longevity risk,

- and legacy.

At this stage, mistakes may become harder to recover from.

The conversation often moves from:

“How do I grow my wealth?”

to:

“How do I preserve, distribute, protect, and transfer what I have built?”

Protection may now serve a different purpose.

Rather than creating an estate quickly, strategies may focus on:

- preserving wealth,

- creating predictable income,

- protecting surviving spouses,

- addressing estate-tax concerns,

- managing longevity risk,

- or helping assets transition efficiently across generations.

This is where insurance, annuities, guaranteed income strategies, tax diversification, and coordinated estate planning may become part of a broader conversation.

Not because any one strategy is always appropriate.

But because different life stages often require different balances of:

- sustainability,

- predictability,

- and cost efficiency.

Supporting Planning Dimensions

While the Ametrine Planning Triangle™ focuses on:

- Sustainability,

- Predictability,

- and Cost Efficiency,

thoughtful financial planning may also involve several supporting dimensions.

These may include:

Supporting Dimension | Financial Meaning |

Growth | Long-term accumulation, purchasing power, and inflation management |

Accessibility | Liquidity, flexibility, and access to assets when needed |

Transferability | Efficient transfer of wealth, assets, or income across generations or beneficiaries |

Protection | Managing, reducing, or transferring financial risks appropriately |

Tax Efficiency | Minimizing unnecessary economic drag and improving long-term net outcomes |

Legacy Planning | Preserving values, continuity, stewardship, and family preparedness |

Income Sustainability | Creating reliable and sustainable income throughout retirement |

Simplicity | Reducing unnecessary complexity where appropriate |

Flexibility | Maintaining adaptability as life circumstances and markets change |

No single financial strategy maximizes every planning dimension simultaneously.

That is why financial planning often requires balancing competing priorities as life circumstances evolve.

Sophisticated Wealth Management Often Involves Coordination

Sophisticated portfolio construction often involves balancing:

- growth,

- risk management,

- tax efficiency,

- liquidity,

- income sustainability,

- and long-term financial objectives simultaneously.

But thoughtful wealth management is often more than simply customizing an investment portfolio.

It may also involve coordinating multiple moving parts across:

- investments,

- taxes,

- protection strategies,

- retirement income,

- estate planning,

- liquidity needs,

- business interests,

- and family responsibilities.

As life stages evolve, financial priorities, risks, and tradeoffs often evolve as well.

This is another reason why thoughtful financial planning may extend beyond simply searching for the lowest cost or highest return in isolation.

Why Wealth Creates Complexity

One misconception about wealth is that it eliminates problems.

In reality, wealth often changes the nature of the problems.

As life becomes more complex:

- taxes may become more complicated,

- family dynamics may become more important,

- outside financial requests may increase,

- legal exposure may rise,

- and preserving wealth may become harder than building it.

This is why sophisticated planning often involves coordination among:

- financial advisors,

- CPAs,

- attorneys,

- insurance professionals,

- investment managers,

- and other specialists.

Successful people often understand this concept in other areas of life.

They hire doctors, attorneys, accountants, engineers, and consultants not because they are incapable, but because they understand the value of expertise, time, coordination, and specialized judgment.

Financial planning is often no different.

Everyone Needs Help With Something

Success does not eliminate uncertainty.

Many successful people still face questions involving:

- aging parents,

- children,

- retirement timing,

- inheritance,

- business transitions,

- taxes,

- healthcare,

- protection,

- and legacy.

Financial confidence does not come from pretending to know everything.

It often comes from:

- asking better questions,

- understanding tradeoffs,

- and seeking guidance where appropriate.

Legacy Is More Than Money

Eventually, financial planning often becomes less about accumulation and more about stewardship.

Questions begin to shift:

- Will future generations be prepared?

- What values should continue?

- How should wealth be transferred responsibly?

- What impact will remain after I am gone?

Legacy is not only about transferring assets.

It may also involve transferring:

- responsibility,

- preparedness,

- values,

- and opportunity.

This is another reason tradeoff thinking matters.

A strategy designed purely for growth may not fully address protection. A strategy designed purely for tax efficiency may not fully address family readiness. A strategy designed purely for simplicity may not fully address long-term legacy goals.

Planning often requires balance.

The Ametrine Perspective

At Ametrine Wealth Strategies, we believe financial planning is not about chasing perfection.

It is not about maximizing one variable.

It is not about forcing every client into the same strategy.

It is about understanding which tradeoffs may be appropriate for a person’s:

- stage of life,

- level of risk,

- family responsibilities,

- and long-term objectives.

The Ametrine Planning Triangle™ is designed to help frame that conversation.

Because sophisticated financial planning is often not the elimination of tradeoffs.

It is the intelligent management of them.

Complimentary Review Opportunity

Financial planning is rarely about finding one perfect answer.

More often, it involves balancing:

- sustainability,

- predictability,

- cost efficiency,

- growth,

- accessibility,

- protection,

- and long-term financial continuity.

In some situations, lower-cost and simpler solutions may be entirely appropriate. In others, additional planning, protection strategies, coordination, professional oversight, or risk-management tools may introduce additional costs but may also help address specific financial risks, long-term sustainability concerns, family responsibilities, or legacy objectives.

The key is not simply focusing on cost alone, but understanding what purpose a particular strategy is designed to serve and how that tradeoff may impact long-term financial outcomes.

At Ametrine Wealth Strategies, we believe thoughtful planning begins with understanding:

- what you are optimizing for,

- what tradeoffs may exist,

- and how different strategies may impact your long-term financial sustainability.

If you would like to explore how the Ametrine Planning Triangle™ may apply to your personal financial situation, retirement goals, protection strategies, or legacy planning objectives, we invite you to contact Ametrine Wealth Strategies for a complimentary review or second-opinion conversation.

Schedule Your Complimentary Consultation

Because clarity often begins with understanding the questions before making the decisions.

Final Thought

The familiar phrase says:

“Good, fast, cheap — pick two.”

But the deeper financial lesson may be this:

Sophisticated financial planning is not the elimination of tradeoffs. It is the intelligent management of them.

The goal is not necessarily to get everything simultaneously.

The goal is to understand:

- what you are prioritizing,

- what tradeoffs exist,

- and why those tradeoffs matter for your life, family, and future.

Financial confidence often begins the moment people stop asking:

“How do I get everything?”

And start asking:

“What am I truly optimizing for?”

Important Disclosure

This article is provided for educational and informational purposes only and should not be considered individualized investment, tax, legal, or insurance advice. Financial strategies, including insurance and annuity products, involve costs, limitations, exclusions, surrender charges, liquidity restrictions, and varying levels of risk and guarantees depending on the issuing company and product structure. Guarantees are subject to the claims-paying ability of the issuing insurance company.

Investment strategies involve market risk, including possible loss of principal. Past performance does not guarantee future results. The suitability of any financial strategy depends on individual circumstances, objectives, time horizon, income needs, liquidity needs, tax situation, and risk tolerance. Individuals should consult with qualified financial, tax, legal, and insurance professionals before implementing any strategy discussed herein.

The Ametrine Planning Triangle™ is an educational framework designed to illustrate how different financial priorities may interact across various stages of life and should not be interpreted as a guarantee of financial outcomes, investment performance, tax results, or insurance benefits.

© 2026 All Rights Reserved. Ametrine Wealth Strategies, LLC.